March of this year has proven to be a tumultuous time for municipal bonds, which have sagged under the weight of rising yields and unfavorable market momentum. Investors seeking safety in these traditionally stable assets are left reeling, as the dissonance between municipal yields and U.S. Treasuries (USTs) continues to widen. With a concerning trend of increasing yields across all maturities, municipal bonds paint a troubling picture. Instead of offering secure returns, they now compete with increasingly volatile markets, leaving many to question their reliability.

The latest data indicates that the ratio of two-year municipal bonds to USTs has remained stagnant at 69%. For five-year bonds, it sits at 71%, ten-year at 76%, and the thirty-year leads at 91%. These figures tell a chilling story of waning investor trust, as rising yields suggest that the bond market is grappling with deeper systemic challenges. Investors must recognize that what was once perceived as a safe haven might no longer hold the same allure.

An Exacerbating Selling Trend

The recent selloff of municipal bonds, followed by additional yield increases of up to six basis points, underscores a prevailing theme in the market: the eroding confidence in the financial health of municipalities. Kim Olsan, a seasoned fixed-income portfolio manager, has drawn attention to the “one-way trade up in rates” that has prevailed throughout the month, pointing to deteriorating fundamentals and mounting headwinds. It’s an indication that those in the municipal bond market must consider the broader economic factors at play.

Dealer inventories shot up to a staggering $15.4 billion, marking the highest level since mid-December. This surge indicates a significant distribution challenge, foreshadowing trouble for investors hoping to sell or trade these instruments. The stark rise in inventories speaks volumes about the growing disinterest from potential buyers and stresses that investors must brace for a reality where they might not reap the historically stable returns associated with municipal assets.

The Disturbing Shift in Yield Trends

The current yield trend is also alarming. Generic AAA-rated credits have climbed 60 basis points over the past six months, with raw yields consistently surpassing 3.00%. As Olsan notes, this spell of higher yields raises the question: will investors flock to what was once deemed a reliable asset class? Compounding the worry is the fact that certain high-grade credits are again becoming available with total effective yields (TEYs) exceeding 5.00%.

This repositioning forces prospective investors to grapple with tougher decisions—particularly regarding the yield-haul balance. As opportunities sprout for bonds yielding over 5%, one has to wonder whether high-quality issuers can maintain such attractive yields in the face of shrinking demand.

The Dwindling Appeal of Premium Coupons

While bonds in the longer maturities exhibit yields above 4.00%, they hardly promise security for discerning buyers. With premium coupon structures failing to deliver the stability investors have come to expect, many are compelled to look elsewhere. Yet the nuances of municipal coupon and call structure present a paradox; they offer a brief glimmer of hope for maximizing yield, but even then, the risks abound.

In competitive environments, several issuers have seen blends of callable and non-callable bonds attracting varying interest levels. The bidding war for prime municipal bonds has intensified, yet the allure of such investments might eclipse the degree of risk that accompanies them. For those daring enough to venture, the market’s yield landscape has shifted considerably, underscoring the importance of strategic selection in bond portfolios moving forward.

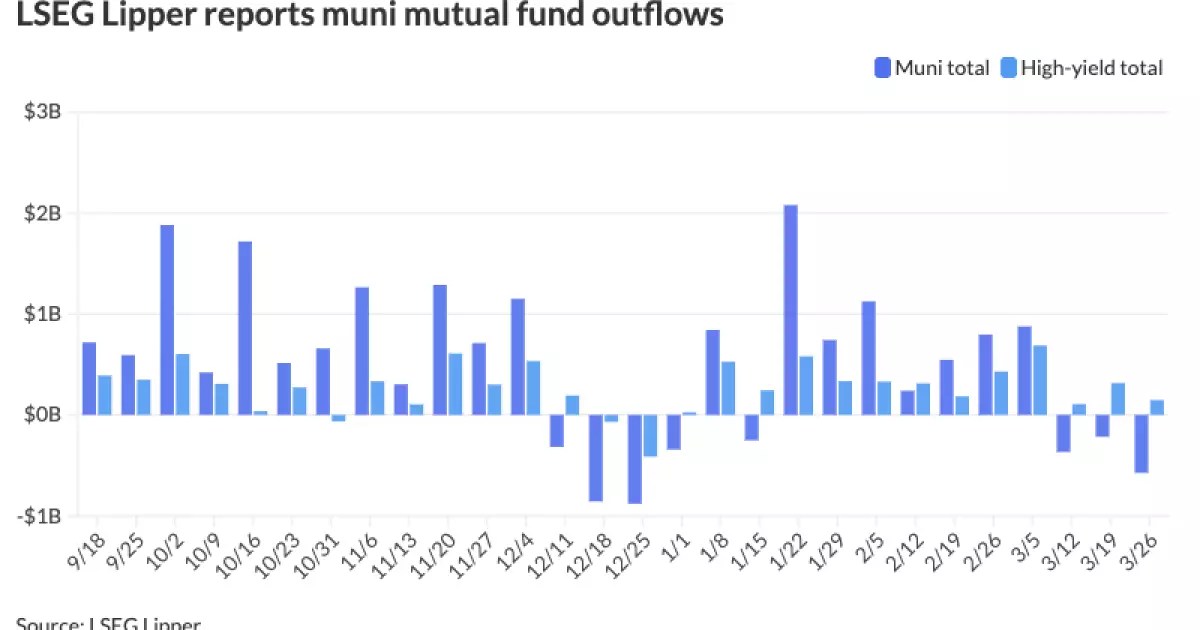

Investor Sentiment and Outflows

Investor sentiment has not escaped this turmoil. Reports indicate a massive withdrawal from municipal bond mutual funds, with outflows reaching $573.3 million—an alarming signal of investor disillusionment as appetite wanes for these once-soothing assets. Tax-exempt municipal funds took a hit as well, with total assets showing significant concentration and risk exposure.

High-yield funds witnessed a brief influx, with a net of $147.7 million pouring in, as investors seek alternatives under duress. But the challenge remains: can they find comparable security amidst such turbulence? The market’s intricacies suggest that, while some sectors may provide positive returns, the municipal bond landscape has undeniably lost its glow.

While the data surrounding municipal bonds may suggest a temporary downturn, the alarming trends are clearly emblematic of larger issues in the market. For the astute investor, navigating these waters requires a discerning lens and a healthy skepticism. As the tension between rising yields and stagnant demand looms large, the call for a re-evaluation of asset allocation grows ever more pressing. In the end, only the bold, informed, and critical investor will emerge unscathed from this turbulent landscape.

Leave a Reply